Private Mortgage Insurance (PMI) is an insurance policy which is paid by the homeowner, and which is meant to protect your lender in case you're unable to make payments on your home in the future.

For conventional loans, PMI is required when a home's equity percentage is less than 20%. This means that PMI can be assigned for purchase money loans and for refinance loans as well.

Private mortgage insurance exists because homes which default are typically sold at auction and may fetch up to twenty percent less than the home's true value because of neglect or damage or worse. The lender, therefore, assumes additional risk when a homeowner's equity stake is small.

PMI offsets this lender risk.

PMI is called “private” mortgage insurance because it's offered by private companies as opposed to the government agencies which insure FHA loans, for example.

What makes PMI different from FHA MIP, though, is that private mortgage insurance will end when a homeowner's equity reaches 20 percent.

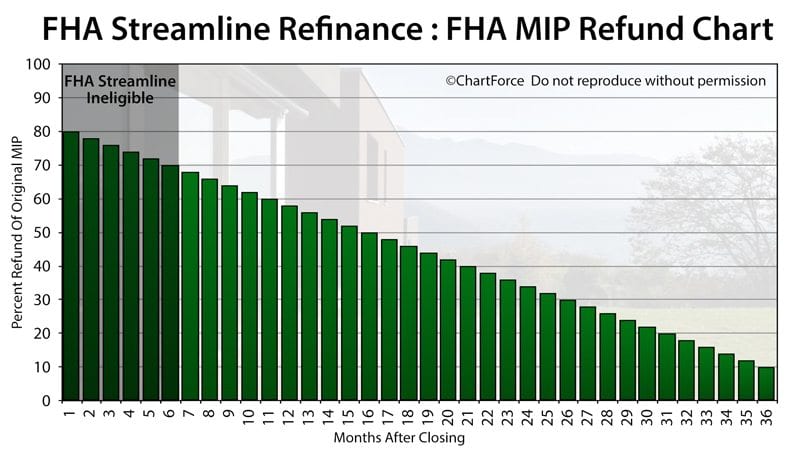

With an FHA loan, the only way to cancel FHA MIP is to refinance.

Private mortgage insurance, like all insurance policies, varies in cost based on your particular risk to the bank. The smaller your downpayment, for example, the higher you should expect your PMI costs to run.

In general, PMI costs range from 30 basis points (0.30%) to 115 basis points (1.15%) of your loan balance annually. Your rate is based on your credit score, your equity/downpayment percentage, and your loan term.

PMI costs are typically paid monthly, divided into 12 monthly installments, then added to your monthly mortgage statement.

However, PMI premiums change regularly. From state to state, and provider to provider, PMI costs will change.

If you know you'll need PMI, remind your lender to comparison shop. Savings could total $10-15 per month.

In general, PMI can be canceled once your loan's principal balance drops to 80% of your home's original appraised value; or, to 80% of your home's current market value.

What If My Current Mortgage Has PMI?

If you are a homeowner who already has PMI, that's okay. You're making an excellent return on your mortgage insurance investment.

Still, you may want to get rid of your PMI, and that's totally possible.

Via a refinance, you can eliminate any type of mortgage insurance as long as your new loan amount is 80% or less of your home's current value.

You can now refinance. The new loan will not require PMI at all.

There are restrictions that sometimes apply, however. Depending on your lender and provider of PMI, you may be asked to show a history of timely payments; a minimum number of payments made (usually 12); or, the absence of a second mortgage.

Lenders are required to update you annually on your PMI cancellation options.

This includes notice of the Homeowners Protection Act of 1998 which required lenders to automatically terminate PMI once the homeowner reaches 78% loan-to-value (LTV), based on the lesser of the purchase price or appraised value from the date of purchase or refinance.

Note, though, that you must be current on your loan when you reach 78% LTV in order to have your PMI removed. If you’re not current at that time, your PMI will be terminated instead on the first day of the first month following the date you get current.

The Homeowners Protection Act of 1998 also states that homeowners are permitted to request PMI cancellation once they 80% LTV, based on the home's original value.

The lender will not contact you, however. You will have to contact your lender.

Private mortgage insurance helps home buyers purchase homes with less than twenty percent down but, despite its benefits, some consumers aim to avoid their PMI at all costs.

For buyers who wish to avoid monthly PMI, there are several ways to go.

The first, and most obvious, route is to make a downpayment of 20% or more. With twenty percent equity, PMI won't apply.

Second, eligible military borrowers can apply for a VA loan which never charges mortgage insurance regardless of your LTV.

Beyond these two options, there are few "cheap" ways out.

Many lenders offer the option of Lender-Paid Mortgage Insurance (LPMI) which is similar to "regular" PMI, except that the lender pays the PMI on your behalf.

In order to pay your PMI, most lender-paid mortgage insurance option require you to accept a mortgage rate increase of up to 75 basis points (0.75%).

This may be suitable to you, but be sure to discuss the LPMI option with your lender first -- especially because LPMI never cancels like borrower-paid PMI does.

Another option is to use "piggyback financing", but this will require a downpayment of 10 percent, usually.

With a piggyback loan, the buyer brings a 10% downpayment to closing and, instead of giving a 90% mortgage to make up the difference, the buyer takes two mortgages, "piggybacked" on one another.

The most common piggyback loan arrangement is an 80% first mortgage, a 10% second mortgage, and a 10% downpayment. This structure is often called an 80/10/10.

For buyers of condominiums, 75/15/10 piggyback loans are more common.

You don't need 20% down to buy a home; and PMI is not a terrible thing.

The best option is to talk to a lender with the knowledge that you have options.

Click here to find a knowledgeable lender with the best rates.

A loan backed by the Federal Housing Administration and offered by lenders. It requires just 3.5% down and lower credit scores are okay.

Default is the failure to pay interest or principal on a loan or security when due. Default occurs when a debtor is unable to meet the legal obligation of debt repayment.

FHA MIP is short for mortgage insurance premium and is FHA's "brand" of mortgage insurance. Homeowners pay an upfront and monthly fee for FHA loans.

Basis point (BPS) refer to a common unit of measure for interest rates and other percentages in finance. One basis point is equal to 1/100th of 1%, or 0.01% (0.0001), and is used to denote the percentage change in mortgage interest rates.

The original sum of money borrowed in a mortgage

A second mortgage is a loan that lets you borrow against the value of your home. Your home is an asset, and over time, that asset can gain value. Second mortgages, also known as home equity lines of credit (HELOCs) are a way to put that asset towards other projects and goals.

The relationship between your principal loan amount and the value of your home. For instance, if your home is worth $100,000 and your loan is $80,000, you have an 80 LTV.