Q: I have good credit of about 730. I meet the requirements for both FHA and Conventional 97. I plan to live in the home for 6+ years. Which has lower payments and what is the difference between the FHA loan and conventional loan? Also, what are the rules around closing costs?

-Dave

A: Hi Dave. Thanks for the question. First, let’s start with the main difference between the FHA and conventional loan programs.

Click here to check today's interest rates (Mar 26th, 2025)What is the difference between an FHA and conventional loan in cost and benefits?

For home buyers with limited funds for a down payment, both FHA and conventional loans are available to help facilitate the purchase of a new dwelling.

FHA loans are insured by the U.S. Federal Housing Administration and are offered by FHA-approved lenders.

Conventional loans are not government-insured and are available through many banks, credit unions, and other mortgage lenders.

You may qualify for both, but there are real differences between them, so take the time to understand the advantages and disadvantages of each before making a decision.

Click here to see how much home you can afford now (Mar 26th, 2025)What is a Conventional 97 loan?

Most people have been told that they can’t get a conventional mortgage with less than 10% — or even 20% — to use as a down payment, but that’s not true.

The Conventional 97 mortgage program allows you to put down as little as 3% for a down payment and then borrow the remaining 97%. The 3% can be sourced from savings, grants, Community Seconds mortgages, and even gift funds. The goal of the Conventional 97 loan program is to help people make their home ownership dreams come true, even if they don’t have lots of cash on hand. Conventional 97 loans require Private Mortgage Insurance (see details below).

Here’s what you need to know about Conventional 97 loans:

- You can get a Conventional 97 loan with as little as 3% of the purchase price of a home.

- You must be a first-time home buyer, though you qualify for this as long as you haven’t owned real estate property in the last three years.

- You can qualify for a Conventional 97 loan with a credit score that’s as low as 620. There are limits to the value of the property for which a Conventional 97 loan can be used. This is based on the conforming limit for the county where the home is located.

- You must take out a 30-year fixed-rate mortgage.

- The property must be owner-occupied.

- The property can be a single-unit family home, co-op, condominium or a unit within a planned unit development.

- You will be required to purchase private mortgage insurance (PMI) and continue paying premiums until you have 78% equity in your loan.

What is an FHA loan?

FHA loans are insured by the Federal Housing Authority. These government-backed loans have been available since the mid-1930s for the purpose of helping first-time home buyers with little available cash and lower credit scores to qualify for a mortgage.

Down payments can be as little as 3.5%, and mortgage lenders (who must meet strict requirements and are limited in the closing costs they impose) are more likely to offer attractive terms because the loans are guaranteed by the government.

Your down payment can be sourced from savings or investments, grants, gifts, and employer programs.

The goal of the FHA loan program is to help people who would not typically qualify for mortgages to become homeowners.

Here’s what you need to know about FHA loans:

- You can get an FHA loan with as little as 3.5% of the purchase price if your credit score is at least 580.

- FHA loans do not require you to be a first-time home buyer.

- FHA loans have limited closing costs.

- Borrowers with credit scores between 500 and 579 are also eligible for an FHA loan, though these loans require a 10% down payment.

- FHA loans are subject to maximum amounts determined by type of home and location of the home.

- FHA loans require additional pre-purchase home inspections.

- The property must be the borrower’s primary residence and can be a single-unit family home, co-op, condominium or within a planned unit development.

- You will be required to pay an upfront mortgage insurance premium (UPMIP) of 1.75% of your base loan amount, which must be either paid entirely in cash or financed into the loan. Following this payment, you will continue paying annual Mortgage Insurance Premiums (MIP) for the life of the loan.

- Borrowers must have a debt-to-income ratio of less than 45%.

- You must be employed and have an income history of at least two years.

- FHA loans are assumable.

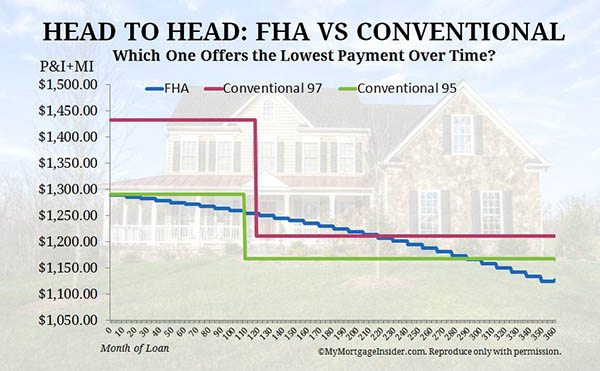

What are the dollars and cents differences between FHA and Conventional 97?

If all things were equal, this would be a simple question. However, there are so many potential variables, including your homebuying circumstances and goals, that the answer is complicated.

If your primary cost concern is about how much you’re going to pay out of pocket to get yourself into a home, and you’ve got a solid credit score, then the Conventional 97 is the way to go. Not only are you able to put down as little as 3% (compared to the FHA’s 3.5%), but you also won’t be required to pay 1.75% for the upfront mortgage insurance premium and there’s a good chance your private mortgage insurance is going to cost less too.

Plus, there’s the additional benefit of having your Private Mortgage Insurance automatically canceling once your loan-to-value ratio reaches 78%.

But things take a quick turn if your credit score falls below 620.

Click here to get pre-qualified to buy a home today (Mar 26th, 2025)When is an FHA loan the right choice?

At first glance, the Conventional 97 loan seems like the clear winner for borrowers with sparse cash to spare. But that’s only when all things are equal.

Once you introduce a lower credit score, all of the variables start to change. Here’s why: The lower your credit score, the higher your interest rate is likely to be for a conventional loan. Once your credit score falls below 620, you no longer qualify for the Conventional 97 loan.

Private mortgage insurance generally costs more than FHA mortgage insurance payments for borrowers with credit scores under 720.

All of this means that if your credit has been negatively impacted, the FHA loan may not only be your better option from the standpoint of your interest rate, it may also be the only one of the two options for which you are eligible.

The hidden benefit of an FHA loan

Whether you’re purchasing a starter home or your dream home, smart buyers will look to the future and whether a property has resale value. That’s where FHA loans offer a hidden benefit not available with conventional loans: the ability for the next buyer to assume the existing FHA mortgage.

As long as a home buyer qualifies for the existing terms of an FHA mortgage, they are able to assume the existing loan and its original interest rate. That means that as interest rates increase, your FHA loan makes your home a much more attractive option. Conventional loans do not provide this benefit.

And if you’re worried abotu FHA lifetime mortgage insurance, keep in mind that you can refinance out of FHA to cancel MI as long as mortgage rates stay at or near current levels. If rates rise too much, a refinance would increase your rate, negating your savings.

Click here to check today’s FHA or Conventional 97 rates (Mar 26th, 2025)Is there a difference in what kind of home you can buy?

FHA and conventional 97 loans limit the amount of money you can borrow, though these limits are determined by different factors and sources.

The FHA sets its limits based on the county in which the home being purchased is located, while conventional loan limits are subject to the conforming loan limit set each year by the Federal Housing Finance Agency.

Additionally, the FHA requires an additional appraisal for homes being purchased using an FHA loan. Though this may feel like an added layer of bureaucracy, the agency’s higher standards are based on adherence to local code restrictions, as well as ensuring the safety and soundness of construction.

FHA loans are not available for homes being sold within 90 days of a prior sale.

Finding the right low down payment mortgage solution for you

With so many factors potentially affecting your personal situation, and so many advantages to each type of loan, choosing the right option can be a challenge.

The good news is that there are plenty of loan professionals who are eager to help you find the solution that’s tailor-made to your needs.

Click here to get a pre-approval now (Mar 26th, 2025)