How interest rates affect buying a home

How do interest rates affect buying power when you’re searching for your next home? Will you have to settle for a less-nice house if mortgage rates rise?

The simple answer is that the higher your mortgage rate is, the higher your monthly payments are going to be.

So, yes. You really will get less home for your money if mortgage rates go up appreciably. That could mean a smaller place, or one in a less desirable neighborhood, or one that needs improvements or upgrades.

See what mortgage rate you can receive with your credit score, income, and purchase price.

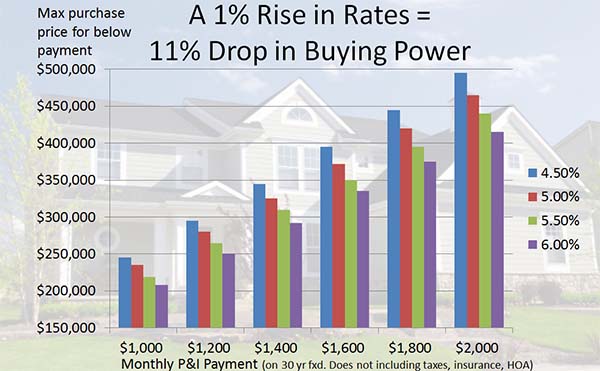

11%! Really?

What most shoppers don’t realize is how dramatically their buying power is diminished with relatively small rate increases.

Let’s imagine you had $1,200 per month to spend on your principle and interest payment. (Keep in mind this number doesn’t include things like property tax, insurance, mortgage insurance, or HOA dues).

That $1,200 per month can go a long way when rates are low. For instance, if you locked in a 30-year fixed mortgage at 4.5%, you could buy a house for $295,000 if you had 20% down. But let’s say rates rise to 5.5%. Still a great rate, but 1% higher than you planned.

Now you are limited to a purchase price of $265,000, again assuming 20% down. That’s a 10.17% reduction in buying power and $30,000 shaved off your maximum purchase price. At $1,800 per month and 20% down, you could buy a home for $445,000 with a 4.5% interest rate. But at 5.5% your maximum home price is now $395,000 – an 11.24% reduction in buying power.

At the lower end of the spectrum, $1,000 per month would buy you a $235,000 home at 5.0% but just a $208,000 home at 6.0%. That’s an 11.49% reduction and in some areas could make the difference between getting into a home or not, or settling for less house.

A rate increase could harm your buying power more than increasing home prices. It’s unlikely home prices would rise by more than 10% in a year, but if rates increase by 1% it will have the same effect for buyers.

High Rates Affect High Loan Amounts the Most

As you move to higher purchase prices, the sheer dollar amount that is shaved off your purchase price by rising rates is pretty incredible.

You could buy a $420,000 home at 5.0% if your budget were $1,800 per month. But at 6.0%, your purchase price is $375,000, a reduction of $45,000.

At a $2,000 per month payment, your maximum purchase price is cut by over $50,000 by a 1% increase in rates.

These are big numbers and could affect your ability to get into the home you wanted, or into a home at all in higher-priced areas.

Choosing when to buy

The simple truth is that if rates go up, you will qualify for less of a home. The 11% shift in buying power is often the difference between an extra bedroom or an older home versus a newer one.

If rates are low enough to make the home you want accessible, it’s best to pull the trigger and buy. Of course, you need to take a look at your economic stability and your plans to stay in one spot for at least 7 years. But, if you’re fairly certain you can handle a home, and rates look good but you’re still waiting, I would advise you to move up your plans to start looking for a home and getting prequalified for a home.

Your options if rates go up

Buying a home while rates are lower is the best option for home shoppers. But there are other options to help other potential homebuyers qualify for the same price point home at a higher rate, including a larger down payment or adding a non-occupant co-borrower to the loan. A 5- or 7-year adjustable-rate mortgage (ARM) — which comes with lower rates for the first five or seven years — might bring a more expensive home back into reach. Another possible option is an 80/10/10 piggyback mortgage which could allow you to finance part of a larger down payment.

Long term rates forecast

It might be a mistake to assume that mortgage rates’ behaviors over the last few years are much of a guide in the long term. Because those have been anomalous by historical standards.

If you spend a little time on Freddie Mac’s archive of 30-year, fixed-rate mortgage rates, you can go back to 1971. And, for most of that time, things were very different from how they’ve been over the last decade.

Since 2010, average rates for these mortgages have remained within a fairly narrow range. Looked at annually, they’ve not gone higher than 4.69 percent or lower than 3.65 percent.

But rates so low are incredibly rare. In fact, they never once dipped below 6.0 percent before 2003. And there were 11 long years, between 1979 and 1990, when they didn’t drop below 10 percent. No mainstream forecasters are predicting a return to those sorts of painful levels anytime soon. But, of course, few would rule out the possibility of rates ever getting back up there.

Chances are, homeowners in the 1980s thought mortgage rates in a 10-18 percent range were the “new normal” — and that lower ones would never be seen again. Those of us living through the 2010s are similarly at risk of seeing today’s low rates as another new normal. And we may be in danger of mistaking a prolonged anomaly for an immovable reality.