Low-income home loan options

You don’t necessarily need a high salary to buy a home. In fact, many mortgage lenders offer loan programs that are designed for people who earn lower incomes.

In this article, we’ll discuss these low-income mortgage loans and their eligibility requirements. We’ll also discuss how different loan programs can help different lower-income borrowers.

Some of these loans help by allowing low down payments. Some can accept borrowers with low credit. And others broaden the definition of “income” to help you qualify.

Check your eligibility to buy a home. Start here (Jul 28th, 2026)

In this article:

- The best low-income mortgage options

- Benefits of low-income mortgage loans

- Tips for buying a home with low income

- Seller-paid closing costs can help

- How lenders decide to approve your loan

- FAQs

- Getting pre-approval

- Final words

- Our recommended lenders for low-income loans

The best low-income mortgage options

There’s more to mortgage eligibility than income, but income matters a lot. Many common mortgage qualifying problems stem from income level. For example, people with lower incomes tend to have lower credit scores and higher debt ratios — two factors that make it harder to get loan approval.

Different low-income home loan programs work in various ways to address different challenges, but they all have the same goal: to help renters become homeowners sooner.

Your best low-income mortgage loan option will depend, in part, on your specific challenges. Let’s take a look:

- Conventional loans: Special conventional loan programs can offer low down payments and helpful ways to document a higher household income.

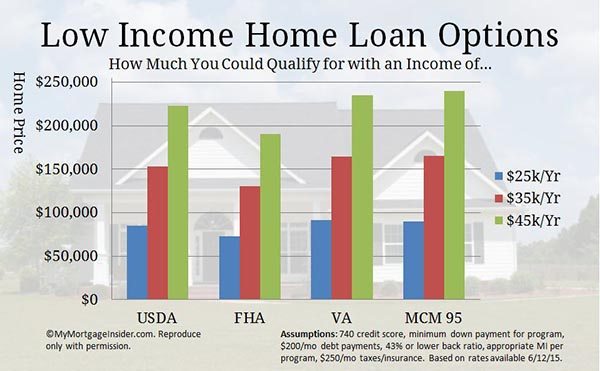

- FHA loans: You’d need to make a down payment of at least 3.5%. That’s $3,500 for every $100,000 in the home price. But people with lower credit scores can qualify more easily.

- VA loans: These are great no-down-payment options for military service members and veterans; however, borrowers without military connections can’t apply.

- USDA loans: These loans require no down payment, drastically lowering your out-of-pocket contribution. But they aren’t available everywhere, and credit qualifications are stricter than most other loans.

- HFA loans: State Housing Finance Agencies specialize in helping low-income borrowers get affordable mortgage loans. A housing agent or counselor can guide you through the entire home-buying process.

- Good Neighbor Next Door: Public servants can buy certain homes at half-price through this program, but inventory is limited.

- Manufactured home loans: Manufactured homes tend to cost less. Lower home prices can help lower-income borrowers buy more affordably.

In addition to these various loan programs, down payment assistance is available through local governments and nonprofits offer special grants and loans to help with your down payment and closing costs. If your hurdle is coming up with enough upfront cash, look for down payment assistance programs near you. More on these programs below.

Now, let’s look at these programs in more detail.

Conventional loans: Loan programs designed for low-income buyers

Conventional loans now include options designed to help low-income buyers with lower down payments.

Both Fannie Mae and Freddie Mac — the two companies that regulate conventional loans — offer mortgages with a minimum down payment of 3% of the loan amount. Fannie Mae’s program is called HomeReady; Freddie Mac’s is called Home Possible.

These loans both work for borrowers who earn 80% or less of their area’s median income. They also allow gifts or down payment assistance grants or loans to cover the required 3% down payment.

Sellers can also pay up to 3% in closing costs, lowering the buyer’s out-of-pocket requirement even more.

And, borrowers may be able to include income from a boarder or renter in the loan application. More documented income can help lower DTI. A lower DTI increases approval odds and lowers the loan’s mortgage interest rate and monthly payments.

Home Possible loans can allow alternative forms of credit history, such as your rent or utility payment history. HomeReady requires a traditional credit history but also can approve buyers with credit scores as low as 620.

These loans require private mortgage insurance (PMI). But unlike government-backed mortgage insurance fees, you can cancel PMI without refinancing. You’ll just need to wait until you’ve paid off 20% of the home.

Check to see if you qualify for a low down payment home loan. Start here (Jul 28th, 2026)

FHA Loan: A great mortgage option for lower incomes

Since 1934, the Federal Housing Administration, or FHA, has been helping lower-income Americans become homeowners.

This government-backed program isn’t designed specifically for low-income buyers. Anyone can apply. But this program tends to help lower-income borrowers through its relaxed credit qualifying rules.

After all, people with income challenges can sometimes also have credit challenges. And, as a low-income home buyer, here are some additional features of an FHA loan that you will be interested in:

- The required minimum down payment of 3.5% can come from down payment gift money

- Credit scores as low as 580 can qualify; with 10% down it’s possible to get approved with a score as low as 500

- FHA has more lenient debt-to-income ratio (DTI) requirements than conventional financing, meaning you might qualify with a lower income

- FHA does not require you to have the extra money in the bank after closing the loan

- You can use a co-signer (another party who contributes to the loan repayment but won’t live in the home)

Like USDA Guaranteed loans, FHA loans come from private lenders and are insured by the FHA.

FHA 203k: Buy and fix up a home with one loan

An FHA 203k loan is an FHA mortgage with an added feature: the ability to finance the purchase price and rehab costs into the mortgage.

This loan program is one of the best low-income home loans because it lets take advantage of lower prices on fixer-uppers.

Because the homes are in need of revitalization and don’t meet the requirements for traditional financing, they may be steeply discounted. This allows those with a lower income to get into a home more easily.

Check your FHA eligibility. Start here (Jul 28th, 2026)

VA loans: The cheapest monthly mortgage payments

If you have military experience, the VA mortgage should be the first low-income mortgage option you check out. It requires no down payment, and the seller could pay all or most of your closing costs.

Unlike other loan types, there’s no monthly mortgage insurance, and that alone can save hundreds per month. No mortgage insurance means you can buy more home with less monthly income compared to other loan types.

And, VA loans are more lenient on debt-to-income ratio and credit score requirements. Many low-income borrowers have used a VA loan to buy their first home.

To be eligible, you must have U.S. military service experience of at least:

- 90 days or more in wartime if currently on active duty

- 181 days or more in peacetime

- 24 months or the full period for which you were ordered, if now separated from service.

- 6 years, if in the National Guard or Reserves

If you are eligible, you could be very close to owning your own home despite currently earning a low income.

The U.S. Department of Veterans Affairs runs the program and insures the loans, but private lenders provide financing, so you’ll need to start by finding a VA-approved lender.

Check your VA home loan eligibility. Start here (Jul 28th, 2026)

USDA Guaranteed Loan: A zero-down loan option

The USDA Guaranteed loan program requires no down payment. It’s available for properties in areas the USDA defines as rural, although many eligible areas are quite suburban. To check out eligible areas, see USDA’s property eligibility map.

This program has been a fantastic home loan for lower-income families over the years. You can buy a home at a lower interest rate with little or nothing out of pocket.

What’s more, the USDA loan is specifically designed for:

- People who don’t already own a home

- Those who make 115% or less of the area’s median income

USDA loans are insured by the U.S. Department of Agriculture, but you’d apply through a private lender.

USDA Direct Loan: For borrowers with lower-than-median incomes

The USDA Direct loan program is open to borrowers in rural areas with very low and low incomes, defined as 50% to 80% of the area’s median income. Unlike USDA Guaranteed loans, USDA Direct loans come directly from the USDA.

Also known as Section 502 loans, USDA Direct loans can offer 33-year or even 38-year terms in some cases. And, payment subsidies are available for those who don’t qualify for the full payment.

To see if your income is within limits, see USDA’s Direct Loan income limits page. Your income must be too low for other loan programs to be eligible. You have to make sure you don’t qualify for a USDA Guaranteed loan before you apply for a USDA Direct loan.

Check your eligibility for a USDA loan. Start here (Jul 28th, 2026)

Housing Finance Agency: Assistance for low-income buyers

Almost all states operate Housing Finance Agencies which exist to help more people become homeowners.

These programs usually offer the types of loans we’ve already discussed, but they can also work in down payment assistance grants and loans for people who qualify.

Some programs require at least one borrower to take a homebuyer education course. Many of these courses are now available online.

To check out local mortgage and down payment assistance options, contact your state’s HFA directly.

Good Neighbor Next Door: Discounts for law enforcement, teachers & emergency personnel

The Good Neighbor Next Door (GNND) program is a special loan type offered by the U.S. Department of Housing and Urban Development (HUD). It allows law enforcement officers, teachers and emergency personnel to buy homes at a 50% discount.

Here’s how it works: You find a home on HUD’s GNND website and make an offer. If more than one person submits an offer, a random lottery is held to see whose offer is accepted.

If you are selected, you must prove that you are an approved type of public worker.

HUD establishes a “silent second” mortgage for 50% of the listed price. But if you live in the home for a full three years (and don’t refinance in that time), that debt is erased.

You can use various types of financing for this program. But if you use FHA, your down payment requirement is only $100.

If you meet the above criteria, this is a perfect low-income mortgage option. After all, you only have to make payments on 50% of the home’s purchase price.

Check your home buying eligibility. Start here (Jul 28th, 2026)

Manufactured housing: Options for mobile home loans

You can find some really low prices on manufactured homes, commonly called mobile homes.

Mobile homes can be a great way to get into a home for less money. They don’t appreciate in value the same way standard stick-built single-family homes do. Still, they can be a great way to break into homeownership.

Just be sure you look only at homes built on or after June 15, 1976. Any mobile home built prior to this date can’t be financed with any traditional loan.

Also, to get a mortgage (and not a more expensive personal loan) the manufactured home must be permanently placed on a foundation.

An FHA loan is the often easiest way to finance a mobile home purchase. Standard FHA rules apply, like 3.5% down and lower credit standards, but there are some additional property inspections required.

Check your eligibility for a manufactured home loan. Start here (Jul 28th, 2026)

Down payment assistance programs from charitable & government organizations

When you have a low income, it can be tough to save enough to buy a home. But you’d be surprised how many cities, counties, and states, offer down payment assistance to low and moderate-income home buyers. In fact, there are too many to list.

Down payment assistance, otherwise known as DPA, is a powerful tool for homeownership. It eliminates years of scrimping and saving for a down payment.

Down payment assistance from cities, states, and counties

Many local governments offer DPA funds to lower-income borrowers. Down payment assistance programs revitalize urban and suburban areas. These gov programs encourage families to buy homes, move in, and improve the community.

Here are some examples of down payment assistance available:

- Orlando, Florida: $40,000

- New Jersey: $15,000

- Connecticut: $20,000

- Seattle, Washington: $55,000

- St. Louis, Missouri: $6,000

Each program is a little different. Sometimes the down payment assistance is a low-income grant that you don’t have to repay. Other DPA programs lend you money at little or no interest but need to be repaid eventually.

Ask a local real estate agent about down payment assistance programs in your area, and see our down payment assistance page for more examples of organizations that participate.

Charitable organizations

Some charitable organizations are able to contribute down payment assistance funds toward FHA loans. But, they must be approved by HUD.

To see if a non-government organization in your area is approved, search by name or location here.

See which down payment assistance programs are available to you. Start here (Jul 28th, 2026)

HUD’s HOME Investment Partnership Program

HUD distributes funds each year to jurisdictions in all 50 states to help low-income home buyers. Eligible buyers must make no more than 80% of the area’s median income.

Jurisdictions that administer the funds are too many to list, but you can easily find out if there is a HOME-sponsored program in your area here.

DPA funds can be used in combination with many standard loan types. If there is a program in your area, contact a knowledgeable loan officer to see if you can combine down payment assistance with the loan type you’re interested in.

Click here to check your homebuying eligibility. (Jul 28th, 2026)

Benefits of low-income mortgage loan programs

The biggest benefit of a low-income mortgage loan is so obvious it’s easy to overlook: These programs can help you become a homeowner sooner. Becoming a homeowner sooner gives you more control over your financial life.

Usually, when you don’t own your home, you pay rent. When you pay rent, the rent money lasts a month. It’s like money spent on groceries or gas — essential for the present, but not long-lasting for the future.

Homeownership is different. Your monthly house payment has a bigger purpose than simply keeping your loan up to date. The money also grows a financial asset — the home itself. The more payments you make, the more control you have over the home.

Later, you could borrow against the home’s value. Or you could sell the home and buy another one. Or you could rent the home for extra monthly income. Or, you could simply live rent-free later in life.

For people with lower incomes, breaking into home ownership may feel impossible. The programs we’ve discussed in this article make buying a new home more possible. It’s worthwhile to find ways to take advantage of them.

Pros and cons of low-income mortgage options

|

Pros |

Cons |

|

Achieve homeownership sooner |

Higher annual loan fees |

|

Lower upfront, out-of-pocket expenses |

Fewer loan options |

|

Flexible options address a variety of needs |

May be harder to use in competitive housing markets |

Tips for buying a house with low-income

Even with low-income mortgage loans to help, buying a home is hard when you’re strapped for cash. So, along with finding the right kind of help, you can help yourself by doing the following:

- Work on your credit: Mortgage rates tend to be lower for borrowers with higher credit scores. Try to pay all your bills, especially your debts, on time each month. Try to pay down credit card balances, too

Shopping around: Most mortgage lenders offer most of the same mortgage loans, but mortgage interest rates and loan fees vary a lot by lender. Getting quotes from at least three lenders increases your chances of finding a great deal - Work with an agent: Real estate agents can guide you through the entire process of buying a home, and their expertise may help you to cut a better deal

- Take a class: Mortgage loans are complex, so a lot of first-time homebuyer programs require education courses. Even if yours doesn’t, look for an online education course so you’ll know the basics of borrowing and owning a home (We’ll cover some of those below)

- Ask for help: Your agent, your loan officer, your housing counselor — they’ve all been here before. They can help you make the best decisions and find the right low-income programs

- Get the seller to pay your closing costs: Negotiating for the seller to cover your closing costs could save you several thousands of dollars.

Another big source of help can come from the home’s seller. The seller can help pay your closing costs. That’s a big ask in some housing markets, so we’ll discuss it more next.

Low-income mortgage requirements 2026

Now that we’ve reviewed your tools as a low-income home buyer, let’s dive into the basics of getting a mortgage. These are rules that apply to anyone, with any income, getting any type of mortgage.

Credit requirements

This is the one area of the loan application where you could really shine even if you have a low income. A lender wants to know you’ve been faithful in smaller responsibilities before handing you a big responsibility. It doesn’t matter that your auto loans, credit card limits, and such are smaller than those of higher-income borrowers.

The only thing that matters is that you’ve handled the credit – whatever size – responsibly. This shows lenders your willingness to consistently pay your debts.

A great credit score can raise the total dollar amount you qualify for. If you don’t have a great credit score, you may want to work on that first before beginning your homeownership journey. As a low-income borrower, you need to have all other aspects of your mortgage application in top shape to get the best home available.

Employment requirements

The lender will want to see that you have steady employment, even if income from that employment is low at the moment.

It looks much better on a mortgage application if you’ve had one job over the past two or more years rather than many jobs. The lender wants to know that you can hold down a job since that will be your means of repaying the mortgage.

If you have had a few jobs over the past few years, work up a great letter explaining why you changed jobs. Did downsizing force you to change jobs? Also, tie each employment experience together, stating how each one relates to the other. A long time in the same line of work looks much better than a long history of unrelated jobs.

Debt-to-income (DTI) requirements

The lender will look at how much debt you have compared to your income. If your income is low, you want your debt payments to be low as well.

Here’s why: you are capped at using about 45% of your gross income for your entire housing costs plus any monthly debt.

For example: If you have a $3,000 gross monthly income then 45% of that is $1,350. If you also have a $200 car payment, a $250 student loan payment, and a $50 credit payment, that would leave just $850 per month to cover principal, interest, property taxes, HOA dues, and homeowners insurance on a home.

But if you had just $50 per month in credit card bills and no other debt, you would have up to $1,300 available for a house payment. That’s a $100,000 increase in your buying power because of $450 less in monthly debt.

In the months and years before buying a home, make a plan to pay off as much debt as possible, to lower your debt-to-income ratio and increase your overall buying power.

Down payment requirements

On a tight budget, it can be tough to save money for a down payment. Fortunately, many home loan programs require little in the way of a down payment, which means low-income families can qualify for a home that much sooner.

Still, the lender will want to see that you can save money. So even if it’s only $25 per month, see what expenses you can cut out of your budget to put toward savings for a down payment.

Property requirements

The lender will check out the property to make sure it meets minimum requirements. You might be tempted to look into a fixer-upper to get a lower purchase price that fits within your budget. That’s fine, just keep in mind that loan approval is tough with a beat-up home. Several of the loan programs listed above include basic requirements to ensure the property is safe and livable.

Get pre-approved before looking for a home

To save time and money, get pre-approved before you start home shopping. A pre-approval is a dress rehearsal for your actual loan application. During this practice run, you’ll learn whether you’d get approved for a loan. If you do get the green light, the pre-approval will also show your price range.

With a price range in mind, you’ll know which homes to look at and which ones to ignore. Plus, the home’s seller will know you’re a serious buyer — one who already has the approval of a lender and can actually afford the home.

Check your home buying eligibility. Start here (Jul 28th, 2026)

Low-income mortgage loans FAQ

How can I get a mortgage loan with a low income?

Ask lenders about special programs for low-income borrowers. Also, look for down payment assistance grants and loans in your area. When combined, down payment assistance and low-income mortgage loans become powerful tools for aspiring home buyers.

Do mortgage lending companies finance low-income loans?

Yes, many mortgage lenders offer low-income mortgage loans. These loans work in different ways to address different home-buying challenges. Start by asking about USDA and FHA loans. Conventional HomeReady and Home Possible loans can help, too. Borrowers who served in the military can find great deals through the VA loan program.

What is the lowest income to qualify for a mortgage?

There are no set income levels for mortgage lending. Your lowest income to qualify will depend on your monthly debts, credit score, down payment size, and loan program. However, it’s possible to earn too much to qualify for a low-income mortgage loan. Many of these programs require borrowers to earn 80% or less of their area’s median income.

What is a low-income borrower?

In general, low-income borrowers earn 80% or below of their area’s median income. These numbers are also adjusted for household size.

How can I buy a house with no monthly income?

You’ll need at least some monthly income to buy a home. The income doesn’t have to come from work. It can come from disability benefits or retirement plan payouts. Getting approved for a loan depends on proving you can repay the loan. Income is a huge piece of that puzzle.

How can I afford a mortgage with one income?

Pay down debts and try to save money. This will put you in the best position to qualify for an affordable mortgage. Check out the low-income mortgage programs above to learn ways to increase your likelihood of getting approved.

How do I qualify for a low-income mortgage?

Eligibility requirements for low-income mortgage loans vary by program. In general, improving your credit score, lowering your monthly debts, and saving some money will help.

What programs are available for first-time homebuyers?

First-time buyers can use any type of mortgage loan to buy a home. First-time buyers often benefit from FHA loans because of their relaxed credit qualifying. USDA and VA loans can also help because they require no down payment. The Home Possible and HomeReady conventional programs also help first-time buyers. After you’ve chosen a loan type, look into down payment assistance grants and local tax credits to help cover some costs.

How do I buy a house without proof of income?

Mortgage lenders will need to see proof of income before they approve a loan. If you’re self-employed and don’t have W2 forms or pay stubs, you can submit tax forms or bank statements to show income.

Can I get a grant to buy a house?

Yes, you can find grants to help cover the cost of buying a home. In fact, you could direct low-income public housing vouchers toward the cost of homeownership. Otherwise, grants vary by location. Usually, grants help cover the down payment so you can get approved for a mortgage loan. You’d still need to make the house payments each month.

Can I use a low-income loan to buy a second home?

Most of these low-income home loan programs are designed to help borrowers purchase a primary residence and cannot be used to purchase a second home or investment property.

Final words about low-income home loans

There are many options out there for low-income home buyers. It’s simply a matter of finding the right one. Keep at it. Just because you are denied the first time doesn’t mean you can’t re-apply after you’ve cleaned up your credit, received a raise, or paid off debt.

With some perseverance and knowledge, you’ll be in your own home before you know it. It’ll all be worth it.

Check your eligibility for a low-income home buying program. Start here (Jul 28th, 2026)