Fixed mortgages with shorter terms can create incredible interest savings.

Not a lot of lenders offer short-term mortgage loans. The good news is you can create your own 5-year fixed-rate mortgage and own your home outright in five years.

Click here to check rates on short-term loans (Jul 30th, 2026)

Pros & cons of shorter-term mortgages

But shorter-term mortgages also have a catch: To tap into their interest savings you’d need to make higher monthly mortgage payments.

That’s why 30-year mortgages remain the most popular loan type. Home shoppers who can easily afford a 20, 15, or 10-year mortgage’s higher payments may wonder about the savings a 5-year mortgage could provide.

Who offers 5-year mortgages?

“I don’t know anyone who sells them,” says Chris Thomas, loan originator at America’s Mortgage LLC in Wheat Ridge, Colo.

You might be able to find a 5-year fixed refinance home loan somewhere. But they are rare since most consumers need the lower monthly payments a 15- or 30-year mortgage provides.

Local banks or credit unions in your community might be able to help you since they have more flexibility and power to customize loan terms. Mortgage brokers who work with many different lending sources might also be able to find the right 5-year mortgage loan out there for you.

Create your own 5-year fixed mortgage

If you can’t find a 5-year fixed mortgage loan, you could still create the same savings strategy by getting a longer-term loan and paying more each month. You’d get the loan paid off early while claiming significant savings in interest.

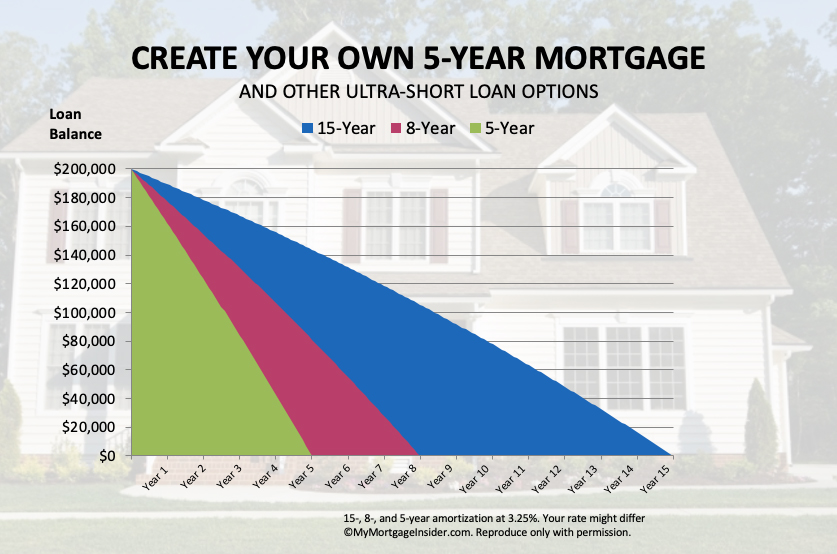

For instance, if you took out a 15-year fixed loan for $200,000 at 3.25 percent, your monthly principal and interest payment would be $1,405.

Even though it’s a 15-year loan you could make larger monthly payments to knock out the balance in five years. To do this you’d need to add an extra $2,211 a month — making your mortgage payment $3,616.

How much could you save in interest by doing this? Over $36,000. Plus, you’d own the property outright 10 years sooner.

Conventional loans let you pay as much extra principal per month as you want without penalty. The end result is essentially a 5-year fixed-rate mortgage.

And this approach has another benefit: Flexibility. To keep this loan up to date, you’d be required to pay only the original payment of $1,405 per month.

So if you had an unexpected financial challenge, you wouldn’t be stuck trying to pay $3,616 a month to keep a 5-year loan up to date.

Keep in mind these payment quotes do not include homeowners insurance, property taxes, private mortgage insurance premiums, or other fees you may need to add on.

Other ultra-short loan terms

Quicken Loans offers an 8-year fixed-rate mortgage through its YOURgage program. This loan program allows borrowers to choose any loan term from eight to 29 years. Quicken’s 8-year terms option was the lowest fixed-rate term we’ve found from lenders online.

How much do you save with an 8-year loan? Let’s say a borrower takes out a $200,000 mortgage on an 8-year fixed-rate loan at 3.25% percent and 70 percent loan-to-value (LTV), the payments would be around $2,350 monthly.

When you compare that to a 30-year fixed loan at 3.5 percent, the cost would be about $900 per month.

(These are hypothetical rates and not ones displayed on Quicken’s site. Your rate might be different.)

This creates a huge difference in monthly mortgage payments — $2,350 for the 8-year loan vs. $900 for the 30-year loan. But the savings in interest from making such a big payment would be astronomical:

- 8-year term: $29,000 in interest

- 30-year term: $123,000 in interest

That’s a savings of $94,000 to borrow the same loan amount of $200,000.

Remember, you can achieve similar savings by getting a longer-term mortgage and paying a lot of extra cash on the principal each month. You don’t have to lock in an 8-year fixed-rate mortgage.

The other kind of 5-year mortgage: The adjustable-rate mortgage (ARM)

Most mortgage lenders do offer 5-year Adjustable Rate Mortgages (ARMs). The rate is fixed for five years, but then the rate can go up if you still have the loan by then.

Keep in mind that the loan isn’t paid off after 5 years — that’s just when the interest rate starts to fluctuate.

ARM loans leave borrowers vulnerable to potential increases in rates – and sometimes large increases — depending on market conditions when the introductory 5-year rate expires and depending on the ARM’s rate caps.

“We try to talk everyone out of getting ARMs right now because the index — which used to determine the interest rate after it changed — is based on short-term interest rates,” Thomas says.

“When inflation kicks in, the rates are going to go up,” he says.

The ARM loan’s new rates are determined by taking the index (whatever that happens to be when the rate changes) and adding a margin. That margin is usually 1.75% for Fannie Mae or Freddie Mac loans, but it could be more, depending on the loan.

The total of those two numbers (index + margin) equals determines the new interest rate after the ARM’s introductory lower interest rate expires, Thomas states.

For instance, if you take out a 5-year adjustable-rate mortgage, the loan has a fixed rate for five years. Let’s say that the initial rate is 3 percent. Now fast forward five years. The loan’s margin is 1.75% (which never changes) and the index has risen to 2.5%. The fixed-rate of 3 percent would become a variable rate of 4.25 percent.

Click here to check adjustable mortgage rates. (Jul 30th, 2026)

Rate caps on 5-year adjustable mortgages

“After the first 5 years is up, the rate can change once a year or once every six months, depending on the loan product,” Thomas says. “The amount it changes depends on the caps.”

There are three caps for every ARM loan:

- Initial cap: The first cap tells how much the rate can change the first time it changes — after the intro rate expires.

- Subsequent cap: The second cap tells how much your rate it can change every time after that.

- Lifetime cap: The third cap tells how much the rate it can change over the life of the loan (the maximum amount it can change).

As an example, if the caps are 2/2/5, your loan’s interest rate could change 2 percent after the introductory interest rate expires. Then it could change 2 percent every year after that (assuming it only changes once a year). The most it can ever change from the original rate is 5% percent.

“In my experience, no one ever asks about the index, the margin, or the caps,” Thomas says. “Most lenders probably don’t even know what those terms mean.”

“People only think about the fact that they can save a little bit of money to start, and that is not the way to think about a loan that is going to last for 30 years,” he adds.

Fannie Mae requires a minimum 5 percent down payment on ARM loans for purchasing a primary residence. You’d need to make a 10 percent down payment if you’re getting an ARM to finance a second home.

Click here to see today's low mortgage rates (Jul 30th, 2026)

5-year ARM rate comparison

Typically a 5-year ARM offers a lower interest rate than a 30-year fixed-rate mortgage. But with current mortgage rates hovering around historic lows, today’s 5-year ARM loan intro rates have aligned more closely with 30-year fixed rates.

So who would be a good candidate for a 5/1 ARM with its variable rate after the first five years?

“I would say that the only people who should get one are people who absolutely, positively know that they are going to sell the house before the rate changes,” Thomas says.

“ARMs are designed to go up,” he says. “The industry term for the initial interest rate is the ‘teaser rate.’ he says. Lenders are teasing consumers into thinking they are getting a good deal, and they are not.”

Check mortgage rates for short-term loans

Home buyers and refinancing homeowners can benefit from today’s low mortgage interest rates. Whether you are looking for a short-term fixed-rate, or an adjustable-rate with an initial fixed period, rates are ultra-low.

But always remember: Along with the market, your mortgage rates will depend on your personal financial situation and borrowing decisions:

- Credit score: Improving your credit score will help you access today’s best rates on all types of mortgages.

- Down payment: Your down payment will help determine your interest rate, too. A larger down payment can lower interest rates and open up more loan types.

- Discount points: By paying more cash upfront you can lower the annual percentage rate for the life of your loan. One point costs 1 percent of your loan amount and lowers your rate by 0.25 percent.

- Loan type: If your credit score doesn’t qualify you for a conventional loan with low-interest rates, consider an FHA loan, USDA loan, or VA loan. With government backing, these loans can offer more competitive rates primarily for single-family primary residences. VA loans are open only to veterans and active-duty military members.

Click here to start your 5-year mortgage rate quote request (Jul 30th, 2026)

Calculating your actual monthly payment

Your monthly mortgage payment depends on your interest rate, loan amount, and loan term. Before going under contract on a home, spend some time with a mortgage calculator, experimenting with different mortgage terms.

If you can’t afford the payment on a 10-year or 15-year mortgage, consider going with a 20-year or 30-year term which will offer lower monthly payments.

As you consider these estimates, remember that your actual monthly payment will likely be higher than the calculator shows because of extra charges such as:

- Homeowners insurance premiums: Most loan servicers let you pro-rate your annual homeowners insurance premiums into 12 installments added to your mortgage payment. This money goes into escrow and will be ready when your homeowners policy comes due.

- Local property taxes: Loan servicers will also collect your annual city or county property taxes as monthly installments paid into escrow.

- Mortgage insurance premiums: Depending on your loan type and down payment size, you may need to buy mortgage insurance which provides protection for your lender in case you default on the loan.

- Other fees: It’s possible to add homeowners association dues or home warranty premiums onto your monthly mortgage payment.

It’s common for homeowners to pay several hundred dollars in taxes, premiums, and fees each month — in addition to the actual mortgage payment which goes onto the real estate debt.

Closing costs: The other expense for home buyers

Interest rates, loan terms, and extra taxes and fees influence your mortgage for the life of your loan. But borrowers have to deal with closing costs before finalizing a new purchase or refinance.

Closing costs include a lender’s origination fee and home appraisal fee. They also include attorney’s fees for title searches and deed transfers.

Discount points — which can provide a lower interest rate — will also be due at the closing table. VA loans require a VA funding fee at closing.

All in all, it’s not uncommon to pay 2 to 5 percent of the loan’s value in closing costs. For a $200,000 loan, 5 percent adds up to $10,000.

Sometimes you can negotiate with the home’s seller to pay closing costs, especially if the seller is especially motivated to close the deal. Some loan options allow you to finance some or all of the costs.

No matter what type of mortgage and loan term you’re considering, you’ll also need to be prepared to cover closing costs.

Click here to check rates on short-term loans (Jul 30th, 2026)