USDA home loans offer 100% financing, low rates, and affordable payments. These loans are becoming more popular as more buyers discover they can buy a home with no down payment.

But not every home — and not every borrower — will be eligible for this loan program.

To apply for a USDA loan with no money down, you’ll need to meet income eligibility rules, and you’ll need to buy a home in an eligible rural area.

Check your eligibility for a USDA loan. Start here (Jun 21st, 2026)

In this article:

- What is the USDA loan program?

- Who is eligible for a USDA loan?

- USDA home loan requirements

- USDA loans and mortgage insurance

- How does the USDA loan compare to other loan types?

- Other differences between USDA and other loans

- USDA home loan FAQs

- Our recommended USDA lenders

What is the USDA loan program?

The U.S. Department of Agriculture (USDA) operates two home loan programs to help low- and moderate-income families in rural areas become homeowners.

Here are the types of USDA home loans for buying existing homes:

- USDA Guaranteed Loan Program: Mortgages issued through this program actually come from private lenders. The USDA’s role is to guarantee mortgage loans. That way, moderate-income borrowers can get lower mortgage interest rates and make no down payment

- USDA Direct Loan Program: The USDA itself issues these mortgages to low-income applicants with standard fixed interest rates of 4% — and rates as low as 1% for some borrowers

These loans help individual borrowers, but they also help rural communities by increasing the demand for single-family housing, sparking economic development

Since its inception in 1949, the USDA Rural Development loan has helped millions of Americans buy housing with little or no money down.

Check your eligibility for a USDA loan. Start here (Jun 21st, 2026)

Who is eligible for a USDA home loan?

Not everyone can apply for a USDA loan. That’s because, unlike FHA loans and conventional loans, USDA loans have eligibility requirements that include rules about location and income.

Here’s how these limits work:

USDA Guaranteed Loan Income Limits

USDA Guaranteed loans are available to “moderate” income earners, which the USDA defines as those earning up to 115% of the area’s median income.

For instance, a family of four buying a property in Calaveras County, Calif., can earn up to $104,650 per year and still get a Guaranteed Loan. If the family earns more, it’ll be ineligible to apply.

Income limits vary by ZIP code and household size. Look up your area here. Typically, moderate earners find they are well within limits for the program.

Keep in mind, the USDA considers all the household income — not just the borrowers’ income. For instance, a family with a 17-year-old child who has a job will have to disclose the child’s income for USDA eligibility purposes.

The child’s income won’t affect whether lenders approve the borrower — just whether the household is eligible to apply for the USDA program.

Check your eligibility for a USDA loan. Start here (Jun 21st, 2026)

USDA Direct Loan Income Limits

USDA Direct Loans — which come directly from the USDA instead of from a private lender — enforce lower income limits than Guaranteed Loans.

For example, that same four-person household in Calaveras County, Calif., must earn $72,000 or less a year to get a Direct Loan.

Look up your area’s income limits here. When you find your county or city and your household size, look for its “low income” number. That’s the number Direct Loans use. (Guaranteed Loans use the “moderate income” number.)

USDA Mortgage Eligible Geographic Areas

To use USDA financing, your new home must be located in a USDA-eligible area. You can search USDA’s maps to browse certain areas or pinpoint a specific address. Just enter the home’s address in the search bar.

More locations than you might think are USDA-eligible. In fact, about 97% of the United States’ land mass is eligible, representing about 110 million people. Some properties in suburban areas outside large cities may be eligible for USDA financing. It’s worth checking, even if you think your area is too developed to be considered “rural.”

The USDA eligibility maps are still based on population statistics from the Census in the year 2020. Maps can change as population data changes.

Check your eligibility for a USDA loan. Start here (Jun 21st, 2026)

Upcoming Eligible USDA Map Changes for 2024

The USDA eligibility map changes with each Census every 10 years. The eligibility map can also change between Censuses as the USDA considers local and state population studies.

Because of these changes, it’s possible an area may appear eligible on the map even though it’s no longer eligible for USDA loans.

To determine, for certain, whether a home is still eligible before starting the application process, check with a USDA loan officer here.

USDA Home Loan Requirements: Eligibility vs Qualifying

The geographical and income requirements we’ve discussed so far determine who can apply for a USDA loan. They don’t determine whether applicants get approved for the loan.

Borrowers who are eligible for USDA borrowing still have to qualify for the loan by going through their lender’s underwriting process. Their income, debt-to-income ratio (DTI), and credit score will help determine whether their loan application qualifies.

Likewise, the home itself will have to qualify by falling within the USDA’s loan limits and by meeting the agency’s property guidelines.

Here are some details about qualifying:

Credit Score Requirements – Updated for 2024

The USDA recommends private lenders who underwrite no-money-down Guaranteed Loans accept credit scores of 640 or higher.

But lenders have some leeway here: They could allow a borrower with a 630 credit score, for example, if that borrower’s application is strong otherwise. Or they could require borrowers to have a credit score of 680 if the borrower’s loan file shows weaknesses.

For Direct Loans, the USDA itself is the lender. The government agency doesn’t set a minimum credit score requirement, but it will make sure borrowers can afford the loan payments before approving the loan.

Debt-to-income ratio (DTI) maximums – Updated for 2024

Borrowers have to prove they can afford the loan’s monthly mortgage payments. This proof comes from comparing the borrower’s income to the borrower’s existing debt load. Lenders call this comparison a debt-to-income ratio, or DTI.

For example, someone who earns $5,000 in gross monthly income and owes $2,000 a month in debt payments — including the new house payment — has a DTI of 40%. A 40% DTI is just low enough to qualify for a USDA Guaranteed Loan. Lenders typically won’t allow DTIs higher than 41%.

For Direct Loans, the USDA, acting as a lender, doesn’t use terms like DTI. But, again, the USDA will make sure borrowers can afford their monthly payments.

Check your eligibility for a USDA loan. Start here (Jun 21st, 2026)

USDA loan limits – Updated for 2024

USDA loans must fall within maximum loan limits for the area. This map will show your area’s maximum loan size for a no-money-down USDA Guaranteed Loan.

Once again we’ll look at that family of four in Calaveras County. That family could get a loan as large as $832,750. Loan sizes vary a lot by location since house prices vary so much by location. In San Francisco County, for example, a USDA Guaranteed Loan could reach up to $1,249,125.

USDA property requirements – Updated for 2024

Homes financed through the USDA loan program must meet the USDA’s requirements for the condition of the property. This excludes most fixer-uppers. The home must:

- Be structurally sound

- Be free of environmental hazards like lead paint

- Have access to water and electricity

- Have a working HVAC system

- Have a working plumbing system

- Have a roof that will last at least two more years

- Have windows and doors that open and close

A USDA appraiser will visit the home to make sure it meets the USDA’s property eligibility rules.

A home that doesn’t meet the USDA’s property requirements may still be eligible for a USDA Rehab Loan. This program can roll the home’s purchase price and its renovation costs into one loan.

USDA loans and mortgage insurance

Most borrowers have to pay for mortgage insurance to get their mortgage approved. Mortgage insurance protects the lender in case the borrower quits making payments and defaults on the loan.

Officially, USDA loans do not require mortgage insurance. But they require something very similar that serves the same purpose: The USDA Guarantee Fee.

About the USDA Guarantee Fee

The USDA Guaranteed Loan Program guarantees the lender it won’t lose money on your loan. (‘Guaranteed’ does not mean that every borrower’s approval is certain; the guarantee is for the lender.)

But this guarantee still helps the borrower. Backing from a government agency removes much of the risk from the loan and allows banks and mortgage companies to offer a zero-down loan at incredibly low rates.

Borrowers pay for this guarantee through the USDA Guarantee Fee which charges 1% of the loan amount upfront and 0.35% of the loan amount each year.

The annual fee is paid monthly in 12 equal installments. For each $100,000 borrowed, the upfront fee is $1,000 and the monthly premium is $29.

The borrower can roll the upfront fee into the loan amount or pay it out of pocket. Compared to other loan types like FHA, or the private mortgage insurance (PMI) on conventional loans, the USDA mortgage insurance fees are among the lowest.

How do USDA loans compare to FHA or conventional loans?

Most home buyers use conventional or FHA loans instead of USDA loans to buy new homes. Which loan type is better?

How USDA loans compare to conventional loans

The federal government cannot guarantee lenders won’t lose money on conventional loans. Because of this, loan approval depends more on the borrower’s credentials.

So, borrowers who have a big down payment, a high credit score, and a low debt-to-income ratio can often get a good interest rate on a conventional loan. This can save money because conventional borrowers don’t have to pay the Guarantee Fee, and they’ll have more flexible loan options.

But borrowers who struggle to qualify for a conventional loan will usually pay higher interest rates and higher mortgage insurance premiums. These borrowers can often save money with a government-backed loan program like USDA despite its fees and regulations.

Conventional lenders do add a private mortgage insurance premium (PMI) each year but no upfront fee. This annual PMI rate varies by borrower and won’t be charged on loans with 20% or more down.

How USDA loans compare to FHA loans

Like USDA loans, FHA loans have the backing of a government agency. In this case it’s the Federal Housing Administration that insures private mortgage lenders, allowing more affordable borrowing.

Unlike USDA loans, FHA loans have no income or geographic rules. Just about anyone can apply.

FHA loans are particularly good for borrowers with lower credit scores. Someone with a score as low as 580 could still get FHA approved with a down payment of 3.5%. (Borrowers with credit scores as low as 500 must pay 10% down, and not every lender will approve such a loan.)

Compared to the USDA’s credit score limit of 640, the FHA’s rules can be a game changer.

And along with more relaxed credit score requirements, FHA loans also feature more relaxed debt-to-income ratio rules. Some lenders may approve borrowers with DTIs as high as 50%.

However, FHA borrowers pay higher fees: 1.75% upfront and 0.55% annually for most new borrowers.

Other differences between USDA loans and other loans

Here are some other differences between USDA and other loan types:

USDA requires zero down (100% financing)

USDA loans can finance up to 100% of a home’s purchase price. That’s a huge pro that only the VA loan program for veterans can match.

For example, FHA loans require a minimum of 3.5% down payment, adding thousands to upfront expenses. Conventional loans can go as low as 3% down. The USDA’s no-money-down feature has allowed many people to buy a home who would otherwise be locked out of homeownership.

Check your eligibility for a USDA loan. Start here (Jun 21st, 2026)

USDA loan length

The USDA Guaranteed loan offers just two mortgage choices: 15- and 30-year fixed rate loans. Adjustable-rate loans are not available through the USDA. USDA Direct loans offer 33- and 38-year fixed-rate terms, which can lower monthly payments.

FHA and conventional loans offer a wider variety of fixed and adjustable-rate loans. Shorter terms, like a 10- or 12-year loan, require higher payments but charge less interest over time.

USDA mortgage rates

USDA loan rates often come in below conventional and FHA loans. Only VA loans, which only veterans and active duty military members can access, come in consistently lower.

The USDA’s backing — combined with the program’s higher credit score requirements — allows for lower rates.

Still, mortgage rates vary by borrower, lender, and home. Everybody’s rate is personal. Comparing different lenders and loan types should help you find your best deal.

Check your USDA interest rates. Start here (Jun 21st, 2026)

Closing Cost Options

USDA loans allow the seller to pay for the buyer’s closing costs, up to 3% of the sales price. Borrowers can also use gift funds from family members or qualifying non-profit agencies to offset closing costs when they supply this downloadable USDA gift letter signed by the donor.

USDA loans also allow borrowers to open a loan for the full amount of the appraised value, even if it’s more than the purchase price. Borrowers can use the excess funds to pay closing costs.

For example, a home’s price is $250,000 but it appraises for $255,000. The borrower could open a loan for $255,000 and use the extra funds to finance closing costs.

Asset Requirements

Borrowers who don’t have all their closing costs paid for by the seller, or by assistance programs, will need cash to close the loan. They will need to prove they have adequate assets. Two months of bank statements will be required.

There’s also a requirement that the borrower must not have enough assets to put 20% down on a home. A borrower with enough assets to qualify for a conventional loan without PMI will not qualify for a USDA loan.

Check your eligibility for a USDA loan. Start here (Jun 21st, 2026)

One of the Best 100% Financing Options

No-money-down loans are often misleading. In exchange for paying no money down the borrower pays more in interest and fees over time.

Not so with USDA loans. Borrowers can pay nothing down and still get a competitive interest rate and low annual fees.

Anyone looking for a home in a small town, suburban or rural area should contact a USDA loan professional to see whether they qualify for this program.

USDA Home Loans FAQs

Is FHA better than USDA?

For borrowers who want to pay 0% down, USDA loans are better than FHA loans. For borrowers with lower credit scores — as low as 580, FHA loans are better. For borrowers who can afford a large down payment and have a strong credit profile, a conventional loan could be best.

Is it hard to get a USDA home loan?

Borrowers who meet USDA income rules and who live in a USDA-designated rural area are eligible to apply for a USDA loan. Getting approved for the loan usually requires a credit score of 640 or higher, a debt-to-income ratio of 41% or lower, and a reliable source of income.

How long does it take to get approved for a USDA loan?

USDA loan approval times resemble other loan types. Most loans close in 40 to 50 days. Applicants who respond to their loan officer’s questions quickly can speed up close times.

I’m looking to buy a home in a suburban area. Should I still look into USDA financing?

Yes. Many suburban areas across the country are eligible for a USDA loan. Complete a short online questionnaire to find out if your area is eligible.

I thought USDA home loans were only for farms?

That’s a different USDA program. A USDA home loan cannot be used to finance the purchase of an income-producing farm. In fact, homes with low acreage may be more suitable for the program, since USDA may not allow a home if its land value is more than 30% of the total value of the home.

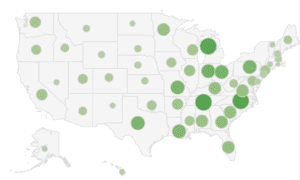

Are USDA Loans Some Obscure Loan Type That No One Actually Uses?

No. Thousands of home buyers use USDA financing each year. These mortgage loans are getting more popular all the time. Below is a map of how many loans were completed in each state in 2015.

Data: CFPB

Does USDA offer a Streamline Refinance program?

Yes. To qualify, the borrower must already have a USDA loan and must live in the home as a permanent resident. The new loan is subject to the standard upfront and annual Guarantee Fee, just like purchase loans. Refinancing borrowers must qualify using current income but may qualify with higher ratios than generally accepted if the payment is dropping and they have made their current mortgage payments on time. If the new upfront fee is not being financed into the loan, the lender may not require a new appraisal.

Can I get a construction loan with USDA?

Homebuyers who wish to build a home with a USDA loan can do so using the USDA construction loan program which combines a construction loan and a traditional 30-year fixed USDA loan into a single-close loan.

Can I buy a new construction home with a USDA mortgage?

Yes. In fact, a new home should meet USDA minimum standards even more easily than will an existing home. Many housing developments are going up in USDA-eligible areas, making this loan a great choice for new homes.

Check your eligibility for a USDA construction loan. Start here (Jun 21st, 2026)

Does USDA require the property to be in good condition?

Generally, yes. The appraiser will state in the appraisal report whether or not the property conforms to minimum standards, which are the same property requirements needed for an FHA loan. Make sure your lender selects an FHA-approved appraiser who can verify the property meets FHA standards.

Can I buy a vacation home with a USDA loan?

USDA loans are intended for the purchase of a primary residence. This type of housing loan cannot be used to purchase a second home.

Can I buy a condo or townhome with a USDA loan?

Yes, however, the lender has to confirm that the condo or townhome meets FHA, Fannie Mae, Freddie Mac or VA requirements. The lender assumes a lot of liability by certifying that a condo project meets these requirements, so they may not be willing to approve a USDA loan for a condo or townhome.

Can I buy a manufactured home with a USDA loan?

USDA typically allows buyers to purchase new manufactured homes only. While pre-existing manufactured homes are typically not allowed, they may be acceptable if the current owner has a USDA home loan on the property. Ask your real estate agent for this information.

New manufactured homes must meet certain thermal performance standards and be permanently affixed to a foundation. It also must have a minimum living space of 400 square feet. A buyer who is interested in a manufactured/mobile home should check with their real estate agent and lender about whether the home is USDA-eligible.

Are USDA home loans only for first-time homebuyers?

No. Buyers who have purchased before may use the USDA program. However, borrowers usually have to sell their current home or prove it’s either too far away from their work or otherwise is no longer suitable.

Check your eligibility for a USDA loan. Start here (Jun 21st, 2026)

Does USDA allow gifts to help with closing costs?

Yes. Gifts can be used provided they are from a relative, charitable organization, government entity, or nonprofit. In some cases, a gift from a friend can be used if proof of the relationship prior to the loan transaction can be established. Applicants receiving a gift will need to complete USDA’s gift letter form. Download the form here.

What’s the minimum credit score allowed for a USDA loan?

USDA grants the highest approval levels to those with a 660 score and above, but the USDA’s recommended minimum credit score is 640.

I have no credit. Can I get a USDA loan?

Borrowers who don’t have an established credit history may be able to qualify for a USDA loan. At least 4 non-traditional sources will be needed, such as:

- Rental history

- Utility payment records

- Insurance payments

Can I finance my funding fee even though my LTV will be more than 100%?

USDA does not consider the Guarantee Fee as part of its loan-to-value (LTV). So in essence, USDA allows for an LTV of a little over 101%.

Why doesn’t every buyer use the USDA home loan program?

Most homebuyers would prefer to do a USDA loan, but perhaps the areas in which they are looking are not USDA-eligible. Larger urban and surrounding areas are not eligible, since the point of the program is to encourage rural development. Still, a surprising number of developed suburban areas are still eligible.

Apply for USDA here

USDA home loan rates are low and free quotes are available now. Check your eligibility for this program and find out about USDA-eligible areas near you. Complete a short online request form to get started.

Check your eligibility for a USDA loan. Start here (Jun 21st, 2026)